Prison Stocks - GEO and CXW

Prison Stocks - GEO and CXW

Recession Proof with Undervalued Assets

The two publicly traded companies in the private prison industry, Geo Group (ticker GEO) and CoreCivic (ticker CXW) have seen their share price fall 75% and 65%, respectively, over the last five years. Reasons for the share price decline are likely related to high debt and interest expenses, COVID-19 disruptions, and fears of political initiatives from elected officials who seek to end the private prison business.

This article is not about political or moral arguments for or against private prisons. All I can say is they provide a service to our government and have no influence on laws or number of people that pass through the justice system and end up as inmates in their facilities. I’m instead interested in discussing the valuation of these businesses.

Aside from the political rhetoric, private prison companies are actually quite boring. They own or manage real estate assets and contract with federal and state entities for daily rates for servicing inmate population in their facilities. Revenues are stable, predictable, and reliable through the economic cycle, including in a recession. There usually aren’t many surprises from quarter to quarter.

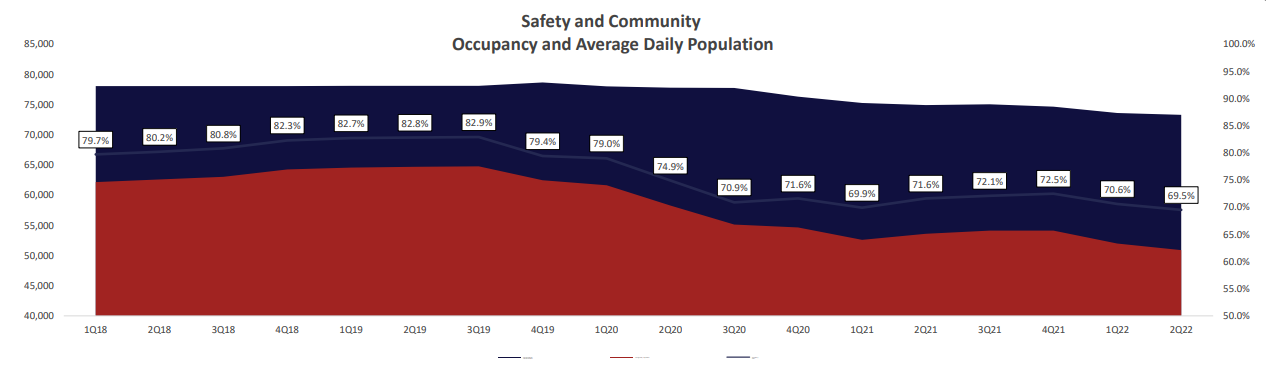

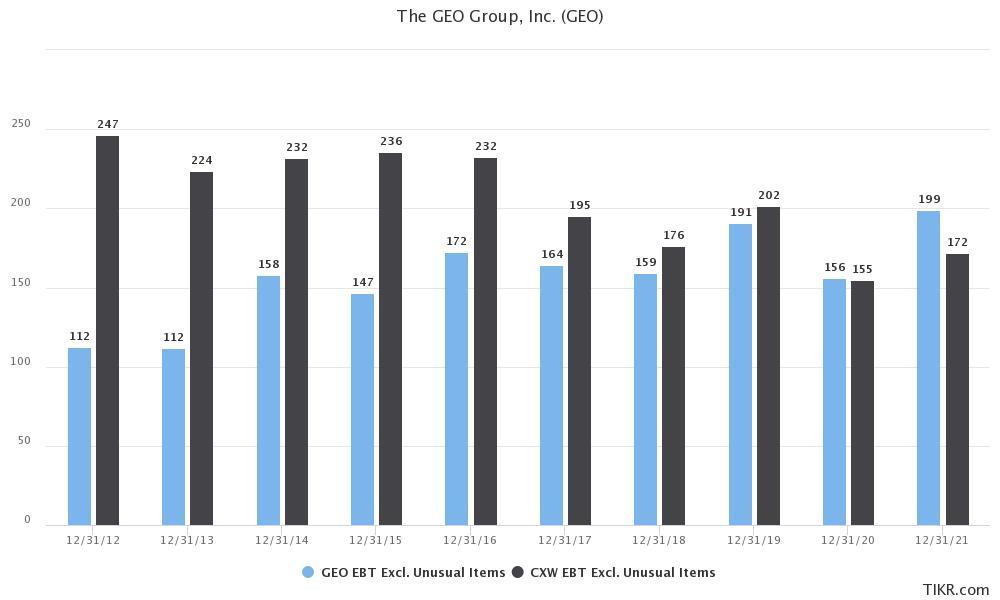

That being said, COVID-19 caused significant disruptions, lowered occupancy rates, and idled facilities. Facilities were court ordered to meet social distancing requirements. Title 42 prohibited undocumented migrants seeking asylum entry to the United States, therefore lowering apprehensions on the Southwest border and utilization of facilities contracted with ICE. As COVID-19 restrictions ease and Title 42 is revoked, occupancy rates will rise again and idle facilities will be re-employed, driving economics to revert to historical levels. Prior to the COVID-19 pandemic, in 2019, both companies generated roughly $200M in pre-tax earnings.

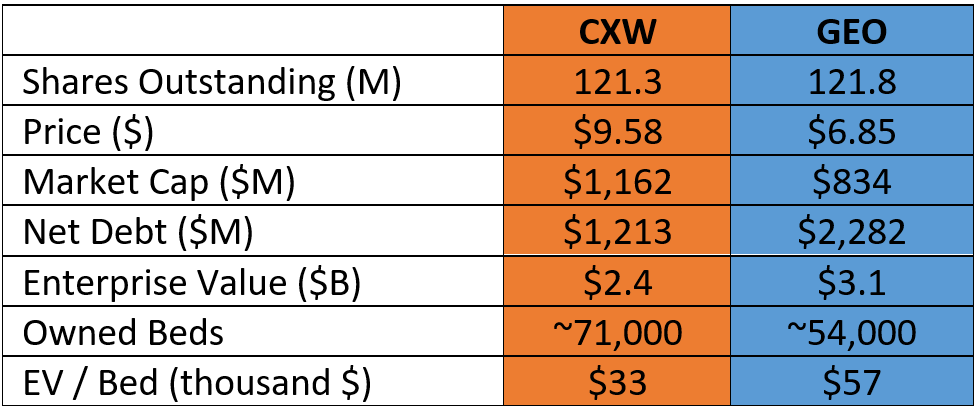

I believe both CXW and GEO are significantly undervalued. Recent asset sale by CXW priced a facility in the state of Georgia for $130M, 2.5x book value, or $66,000 per available bed in the facility. Other smaller facilities have been sold for 4x, and even 9x book value. Current enterprise value implies CXW is trading for a discount to their real estate market value, or $33,000 per bed, 50% of the recent sale value. GEO is more aligned with market value of their real estate assets and trades for ~$57,000 per bed. Also consider the replacement cost of these assets. Recently, the state of Utah completed a new facility by Salt Lake City. The cost ended up at $1.05B for 3,600 beds, or ~$290,000 per bed1.

Both CXW and GEO recently changed their corporate structure from REIT to C-Corp to focus on paying down debt. From the table above, CXW has advanced further in their efforts to tackle debt and has over $1B less net debt compared to GEO. Since the beginning of 2020, CXW has paid down nearly $800M in debt. According to management, their leverage ratio is now manageable and CXW recently initiated a $225M share buyback program to take advantage of their mispriced stock. They’re currently aggressively buying back shares at a rate of $20M per month, annually corresponding to 20% of outstanding shares at current stock price.

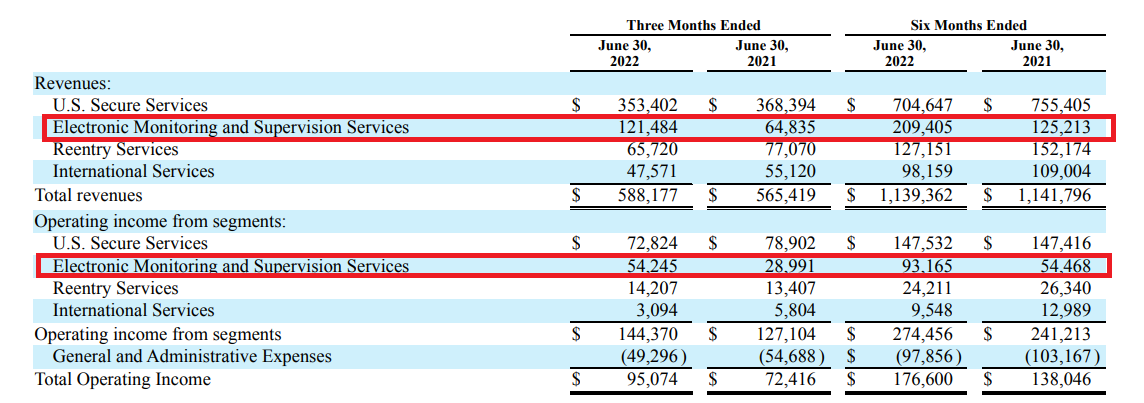

GEO is burdened by higher net debt, totaling ~$2.3B. In addition, the company is currently looking to refinance the debt and stretch out maturities. Interest expenses are expected to rise as a result. Despite the debt and interest burden, GEO has a weapon in their arsenal which makes the debt manageable, BI Inc (BI)., a subsidiary that provides electronic monitoring and supervision services. During COVID-19, government agencies prioritized placement of individuals into non-residential alternatives, including electronic monitoring programs. The electronic monitoring segment has ~45% operating margins, the highest margin segment in GEO’s portfolio. In the first half of 2022, revenues in the segment grew by 70% compared to the first half of 2021 due to higher client and participation count. Despite higher debt and interest expenses, performance of the electronic monitoring segment should continue to drive GEO’s annual free cash flow of over $200M which management will use, along with opportunistic asset sales, to reduce debt.

Rumors started circulating a few months ago about GEO intending to sell BI to pay down debt. GEO bought BI for $415M in 2011 when BI revenues were ~$40M annually. Revenues are now on track to exceed $400M for 2022. Current performance implies BI could be sold to pay down the entire $2.3B net debt amount. Management should be greedy and not desperate about selling, BI is their highest growth and margin segment.

The price of CXW and GEO shares has declined significantly over the last few years due to high debt, political fears, and lower utilization rates resulting from COVID-19. CXW trades for a significant discount to market value of their real estate assets. CXW management is aware of this market disconnect and could buy back 20% of outstanding shares by end of May 2023. GEO trades for roughly the real estate market value, net of debt, but then you get BI for free, which is demonstrating high growth, has 45% operating margins, and is likely worth over $2B based on GEO’s purchase price in 2011. On top you get annual $200+M pre-tax earnings from both companies as facility utilization rates revert back to historical levels.

On a per share basis, CXW costs ~$10, and you get $20-$25 in real estate assets and ~$2 in annual free cash flow. GEO costs ~$7, and you get $20-25 for BI Inc. and real estate assets, and ~$2 in annual free cash flow.

https://kutv.com/news/local/new-utah-state-prison-salt-lake-city-correctional-facility-draper-ribbon-cutting-governor-spencer-cox-corrections